2 min read

RBA Assistant Governor Christopher Kent stated that ‘’the Bank’s policy measures have contributed to the Australian dollar being as much as 5 per cent lower than otherwise in trade-weighted terms (TWI)’’ in his speech on Feb 17[1].

Is RBA overestimating the impact of QE?

QE is supposed to anchor bond yields and this week provided a test with US 10-year bond yields rising. Australian 10-year bond yields rose even more, with the spread with US 10-year yields rising by 23bp since Feb 12.

The RBA appears to be over-estimating the impact of QE on AUD TWI if you believe that the relative size of the central bank’s balance sheet expansion is what matters for the impact on a currency pair[2]. The RBA’s pace of balance sheet expansion (about 5% of GDP rise over 6 months) is barely keeping pace with other central banks, including the ECB or the Fed.

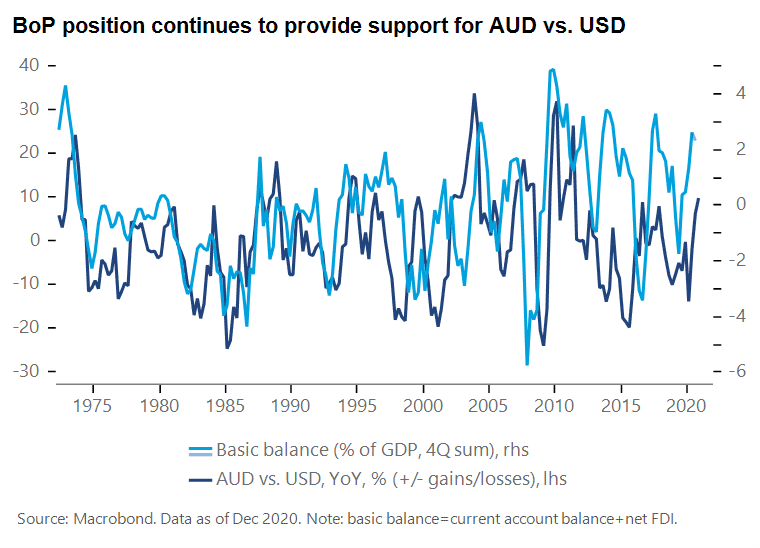

The QE impact on AUD via the portfolio rebalancing effect may continue to be limited by the resilience of Australia’s current account surplus, which portfolio outflows fail to fully recycle. With China not in a rush to return to de-leveraging policies and curb investment, we expect Australian external surpluses to persist.

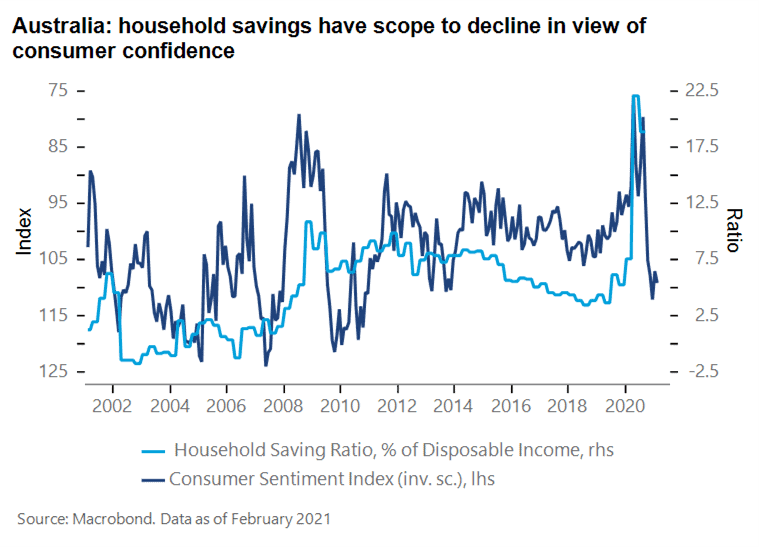

What has so far kept AUD at a discount compared to its terms-of-trade may instead be the domestic risks to the outlook. Compared to other advanced economies, Australia entered the Covid19 crisis with already significant labour market slack, which only worsened last year. Yet as we gauge the ability of economies to return to normal, Australia now seems relatively advanced. As consumer confidence and hiring have rebounded faster in Australia compared to other economies, there is a stronger case for excess savings by households to be spent when the economy fully reopens, which should speed up a reduction of the output gap. In turn, the QE impact on AUD could fade further as the positive differentiation of Australia vs. other developed economies increases.

[1] FX markets around the turn of the year, RBA. Ch. Kent, Assistant Governor, 17 Feb 2021

[2] Does a big bazooka matter? Quantitative easing policies and exchange rates, Luca Dedola, Georgios Georgiadis, Johannes Gräb and Arnaud Mehl, ECB Working Paper, Oct 2020

This post contains the views and opinions of Claire Dissaux as at 19th February 2020 and does not necessarily represent the views and opinions of Millennium Global or any of its Portfolio Managers. The information herein is not intended to provide, and should not be relied upon for any purpose, including investment recommendations or decisions. Portions of the information in this document may constitute forward-looking statements. Due to various uncertainties and actual events, the actual performance of the economy may differ materially from those reflected or contemplated in any forward looking-statement. The information contained in this post is intended for Professional Clients (or Elective Professional Clients) only and does not constitute an offer to buy or a solicitation of an offer to sell, and does not constitute an offer or solicitation in any jurisdiction in which such a solicitation is unlawful to any person to whom it is unlawful. URN: 103870

Taking on the future: Machine Learning in FX Risk Management

By Justin Gang Xu, Head of Risk The global foreign exchange markets are primarily influenced by a combination of fundamental and market dynamic...