2 min read

Japanese Yen - Ministry of Finance Intervention

Japanese authorities have reportedly spent more than 50 billion dollars defending the Japanese yen in the last few weeks. For currency investors, it...

6 min read

2022 was a remarkable year for global markets, with macro volatility back at levels not seen since the mid-1980s and forces conspiring to destroy the concept of the traditional 60/40 portfolio, which experienced its worst performance since the 1930s. Currency volatility also came back with a vengeance, more than doubling over the course of the year, with some significant consequences for international portfolios. Given this macro landscape, we want to break down what has changed in foreign exchange markets, what is driving the return of volatility, and what investors might expect from here.

Why was 2022 such a gamechanger for currency markets?

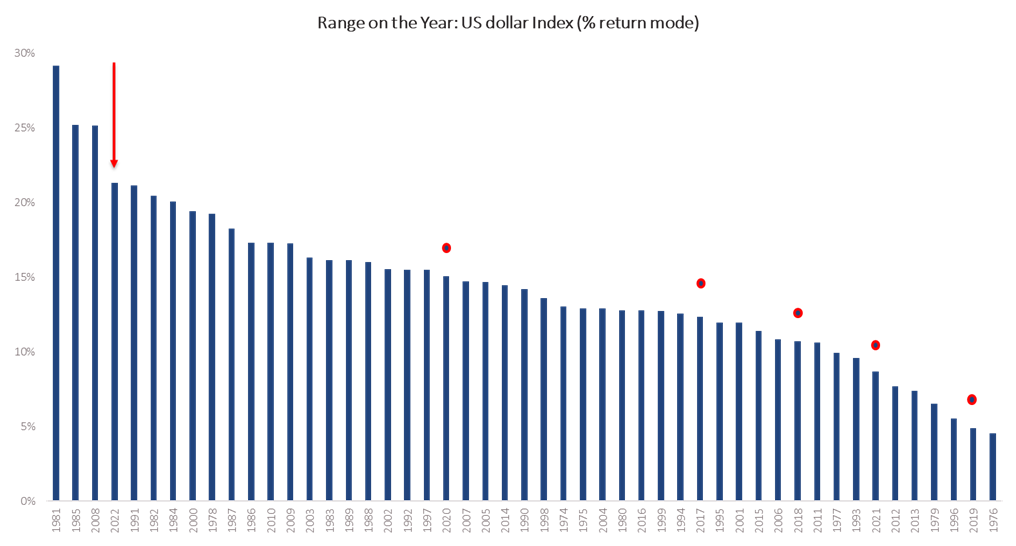

Let’s look at the numbers. If we measure FX market activity by the range of the dollar’s move over a calendar year, in 2022 the DXY experienced its fourth largest range on the year in the last 50 years. To put that in perspective, of the only three years when the DXY saw greater variability, one of those years was the Global Financial Crisis in 2008 and the other was 1985, the year of the Plaza Accord and the greatest monetary intervention we’ve seen in modern financial times. So to the extent the drivers of the DXY’s wide range in 2022 were organic, last year is right up there with the most significant years for foreign exchange in history.

Source: Bloomberg, 1976 to 2022.

And 2022 was not just about the US Dollar: other currencies across developed and emerging markets experienced historically significant ranges as well, including the Japanese Yen with a 34% annual range, the British Pound at 24%, and the Euro at 17%. Meanwhile, the Chinese Renminbi saw a 17% annual range, the Turkish Lira a 46% range, and the Russian Ruble a whopping 71% range.

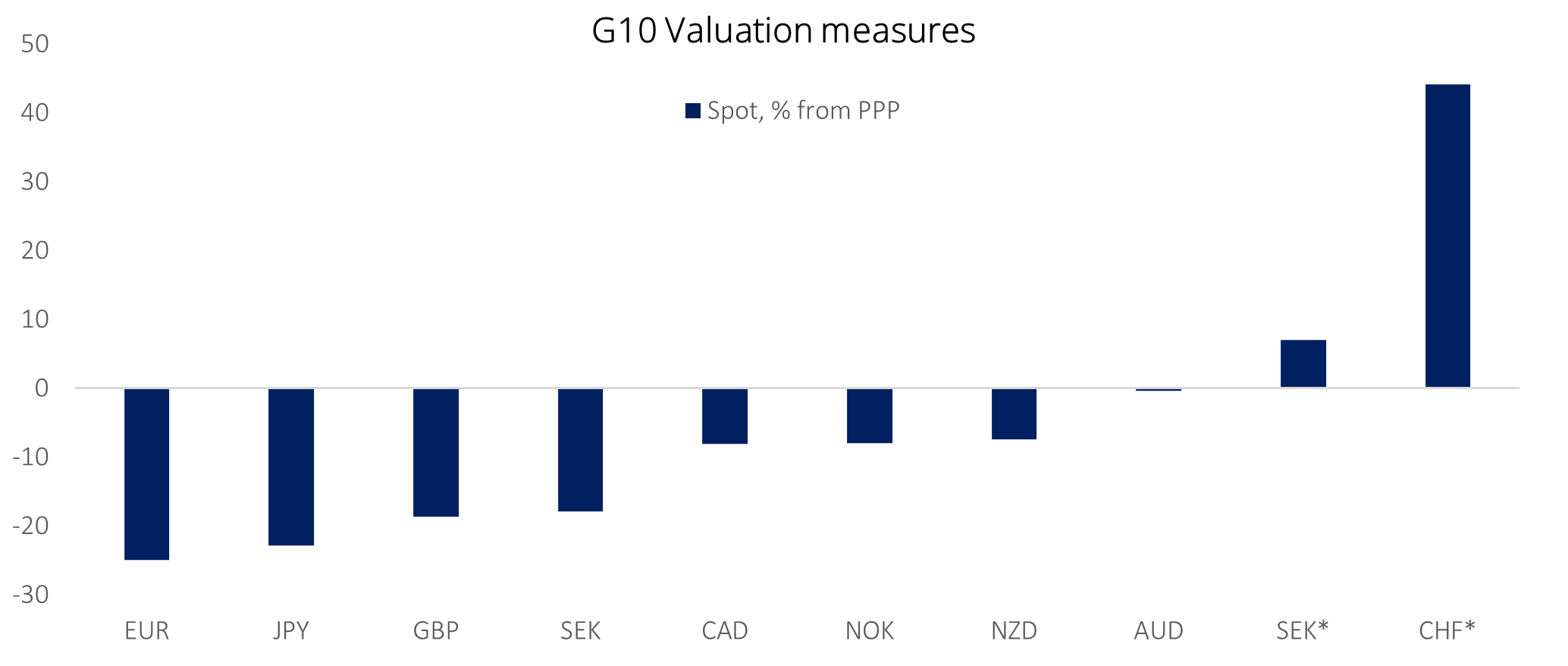

Looking at one-month implied volatility, currency volatility has generally doubled since the middle of 2021 and tripled in the case of some currency pairs, such as USD/JPY. Yet despite this huge uptick in volatility, significant pricing imbalances remain across G10 and Emerging Market currency pairs alike. The Euro remains 25% undervalued against the US Dollar on a PPP basis, the Yen around 22% undervalued against the US Dollar, and the Swiss Franc 45% overvalued versus the Euro, to give a few examples. These lasting imbalances imply we should expect continued significant price action and volatility in 2023.

SEK and CHF vs EUR. Otherwise vs USD. Source: Macrobond, MGI Economics, GS Research. Data as of 7th February 2023.

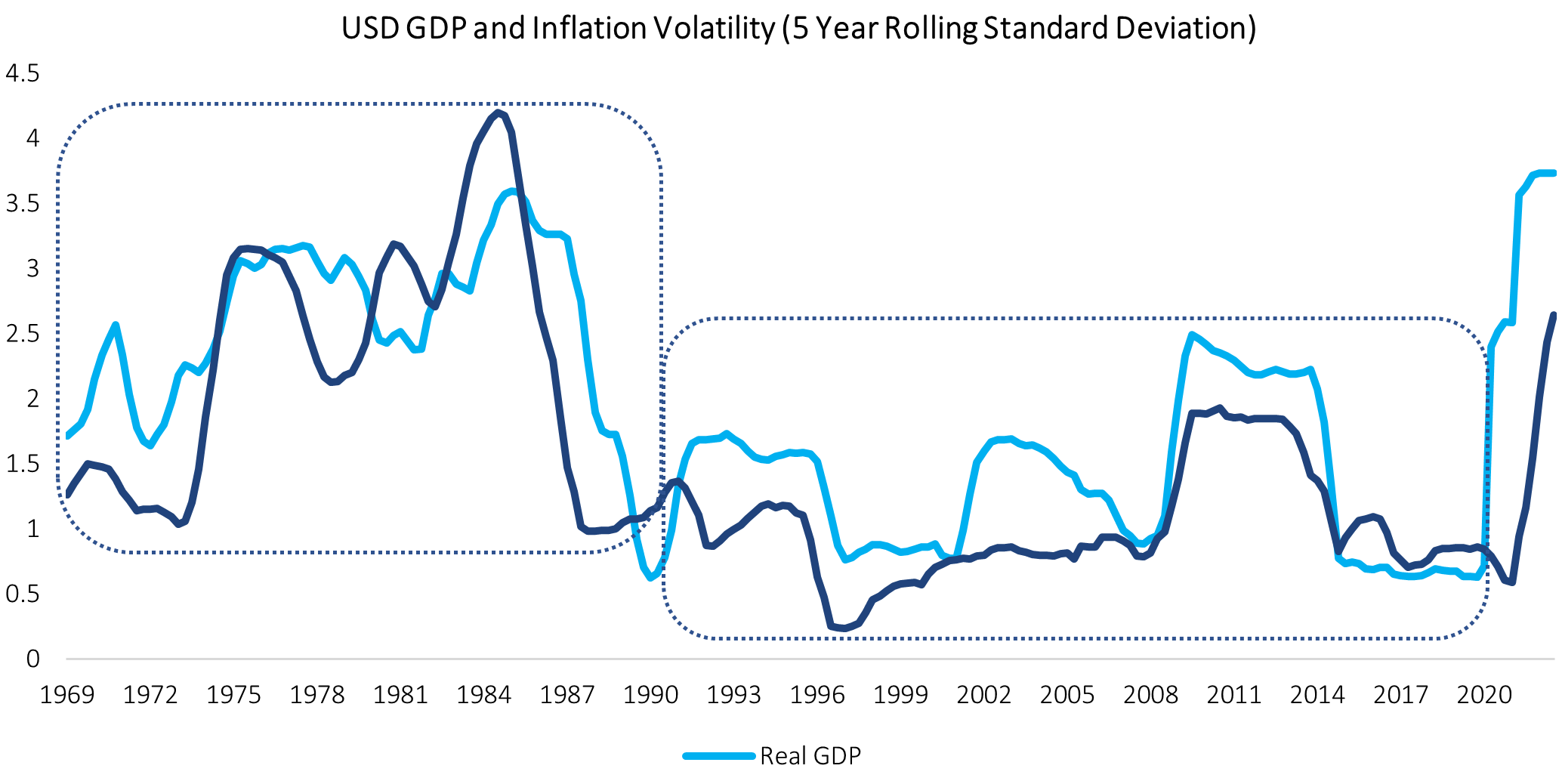

2022 was in our opinion not a flash in the pan for currency markets but rather the beginning of a new regime of heightened macro and FX volatility that we should expect to continue for some time. If we take a longer-term historical perspective, uncertainty in global markets as measured by US GDP and inflation volatility in the late 1960s, ‘70s and early ‘80s was quite high, with numbers approaching 2.5-3% on a 5-year rolling basis. Then came the period of the Great Moderation beginning in the 1990s which saw the volatility of real US GDP and inflation dip down to the 1-1.5% range. We have now entered a new regime more akin to the earlier period, with that macro volatility measurement back around 2.5%. Post-pandemic inflation, global supply chain disruption, and years of monetary largess have all combined to sow the seeds for big changes in the macroeconomic environment.

Source: Bloomberg, September 2022.

However, what we are currently seeing in interest rates is not merely a post-pandemic aberration but a return to historical norms. Despite 2022’s historic rise in rates, the current Fed funds rate is still below the long-term average of the last 50 years, at 4.5%, when the historical average is just under 5%. This suggests that the aberration was not 2022 but was in fact the “race to zero” environment in the wake of the Great Financial Crisis and the post-pandemic period. Now that we are passed that, we are returning to an interest rate environment more akin to historical norms that is likely here to stay for a generation or more. And it’s not just that interest rates are rising: interest rate differentials among countries are widening, further increasing the scope for currency price action.

Fed Funds rate

Source: Bloomberg, November 2022.

Source: Bloomberg, November 2022.

Key takeaways

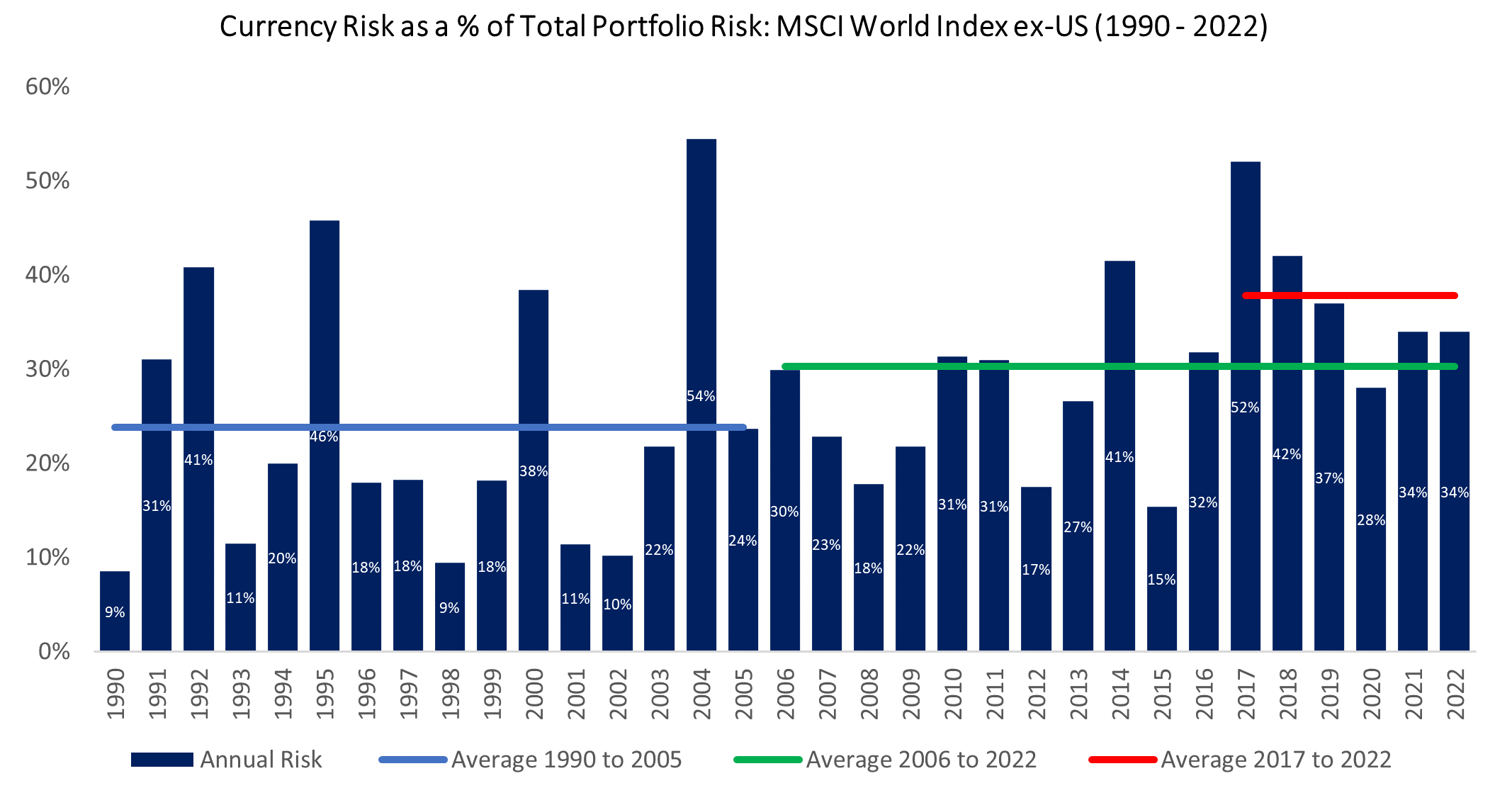

The proportion of total risk in international investments coming from currency is growing substantially. Twenty to thirty years ago, about 25% of the total risk from international equity investments came from the currency component. Over the past 7 years, that percentage of total risk has jumped to anywhere from 30-50%. Given the noticeable increase in the percentage of total risk attributable to currency fluctuations, it is ever more important to focus on that risk and to manage it appropriately. When investing internationally, an investor is really buying two portfolios of risk: 1) the underlying international assets in local currency terms, and 2) the basket of currencies those investments are denominated in. Again, if the volatility of that second portfolio of risk has doubled, the need to manage it should be more pressing.

Heading into 2023, Bridgewater Associates are among asset managers echoing this sentiment. They noted that currency risk is among their top concerns for their clients and that they’re having a lot of conversations with clients on strategic currency hedging, given the heightened impact of FX exposures in this market. They note that over the past year and a half, investors could have seen a different of 30 percentage points of performance depending on their base currency due to these significant moves in the EUR, USD, JPY, etc., suggesting that in this environment, managing currency risk can be as important as managing the underlying assets themselves1.

Source: Millennium Global & Bloomberg, December 2022.

Another consideration in 2023 is the likely deterioration in the outlook for traditional assets. In equities, profits as a percentage of total GDP are at a secular high, particularly in the US, where they sit at 12% versus 6.8% where they were in 1990. This suggests that the prospects for further growth in equity markets are challenged, as inflation will continue to compress margins. Looking at the bond market, we believe, the secular downtrend in bond yields that has lasted almost exactly 40 years is now over. We are at the beginning of a secular shift where yields are likely to trend higher for the coming years. These fundamental challenges to equity and bond markets, as demonstrated by the capitulation of the 60/40 portfolio in 2022, suggest the need for more diversification across portfolios and in particular for more diversified alpha. Currency alpha has the benefit of being both uncorrelated to major asset classes and highly liquid.

What could go wrong?

As we head into February, it is worth examining some of the threats to the now seemingly priced-in Goldilocks scenario, where the Fed engineers a soft landing, inflation goes back to 2% without a hugely disruptive hit to growth, and equity and bond markets begin a sustained recovery. While that scenario is not out of the realm of possibility, it does raise some questions. If the Fed does need to convincingly quash demand to get a handle on inflation, does that square with a mild recession? And if there is a mild recession, is that consistent with the Fed cutting rates in the second half of the year?

The first risk to the Goldilocks scenario is that inflation remains sticky and that even if it comes down this year, we may not get back to 2%, implying the Fed might have to remain tighter for longer.

The other risk is that the economy will prove highly responsive to tighter monetary policy, increasing the chances of a much deeper recession than is currently expected, with what we’ve seen in the mortgage market flowing through to labour markets. This introduces the possibility of a policy mistake by the Fed.

Regardless of how 2023 plays out, we believe longer-term structural inflationary forces are likely to re-assert themselves in 2024+, due to generation shifts in demographic trends, the inevitable slowdown or reversal of globalization in this fractured global economy, and the high cost associated with the global transition to green energy. So even if we win the inflation battle in 2023, the war is not over.

Final comments

We are in perhaps the most uncertain macroenvironment since the end of the Cold War in 1989, which in our view makes a focus on risk-mitigation more important than ever. This applies to all asset classes but in particular to currencies that are so sensitive to macro volatility. Don’t ignore the left-tail risks!

We also expect there to be a premium on diversified alpha in 2023, particularly liquid alpha, given the paucity of returns coming from the traditional 60/40 portfolio and with liquidity drying up in other areas of institutional portfolios. The good news around the return of macro and currency volatility is that it creates ample opportunity for active currency investors to take advantage of these dispersions across macro markets that have generally been lacking in the recent years of quantitative easing.

To download this article as a PDF, please use the form below.

1. Source: https://www.pionline.com/face-face/bridgewaters-rebecca-patterson-currency-risk-geopolitics-key-concern-institutional accessed on 6th February 2023.

The views and opinions contained in this document are those of Abigail Cushing and Mark Astley, correct as at 6th February 2023 and does not necessarily represent the views and opinions of Millennium Global or any of its Portfolio Managers. This information is intended for Professional Clients only, not retail clients. This information does not constitute an offer to buy or a solicitation of an offer to sell and does not constitute an offer or solicitation in any jurisdiction in which such a solicitation is unlawful or to any person to whom it is unlawful. Please see Important Disclaimers on: https://investments.millenniumglobal.com/millennium-global-marketing-disclaimers

2 min read

Japanese authorities have reportedly spent more than 50 billion dollars defending the Japanese yen in the last few weeks. For currency investors, it...

The Euro has become increasingly sensitive to developments between Russia and Ukraine. The main channels through which the ongoing crisis impact the...

We measure the spillover effect that big moves in one currency pair can have on a group of currencies from a purely statistical point of view. We...