11 min read

“Reports of my death are greatly exaggerated” - Mark Twain

Is the twenty-year decline in the proportion of US dollars held in global reserves the beginning of a paradigm shift or part of business as usual?

The topic of de-dollarization has become a hot one in recent months and one around which there is meaningful division of opinion, with doomsayers calling for the dollar's imminent demise and supporters arguing its hegemonic status will be quite hard to undermine and so we shouldn't expect a meaningful change in status anytime soon. Who is right, and what are the stakes for global markets?

Arguments for de-dollarization

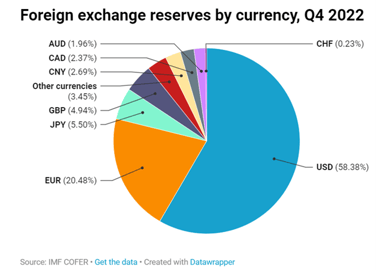

There are a number of reasons why de-dollarization has become a hot topic of late. Perhaps the most immediate is the relatively steep decline we saw last year in the USD’s share of total global reserves. 2022 was not the beginning of this trend but rather an acceleration of a 20-year decline. As of Q4 last year, the dollar’s share of global reserves was 58%, down from 73% in 2001, with the pace of this decline increasingly notable over the course of last year, according to data from the IMF’s Currency Composition of Foreign Exchange Reserves (COFER). After the USD, the euro comes in second place, accounting for about 20.5% of global FX reserves, while the Chinese yuan accounted for just 2.7%.

The dollar’s status is not just about reserves but about trade, and in recent years, countries including China, Russia, Brazil, Iran and some Southeast Asian nations have been calling for trade to be carried out in currencies besides the US dollar. Brazilian president Luiz Inacio Lula da Silva has been one of the most vocal proponents for alternative trade settlement currencies, calling on the BRICS countries (Brazil, Russia, India, China, and South Africa) to move away from the dollar. During an April 2023 state visit to China, Lula asked, "Why can't we do trade based on our own currencies?...Who was it that decided that the dollar was the currency after the disappearance of the gold standard?" (The Financial Times).

We have indeed seen some moves away from the US dollar on the margin, including a move in bilateral Chinese / Brazilian trade to yuan / real invoicing. The yuan has now surpassed the euro to become the second most dominant currency in Brazil's foreign reserves after the dollar as of the end of 2022, according to the country's central bank (Reuters, March 31). Similarly, Argentina announced in April that it will begin paying for Chinese imports in yuan instead of US dollars.

Separately, there has been an increase in central bank buying of gold around the world, which has added some fuel to the de-dollarization fire. Central banks now constitute about one third of all annual demand for gold - the highest level since the 1950s, and we’ve seen the price of gold rise about 20% in the last six months.

Looking at the US domestically, the last few years have bolstered the argument that too much money is being printed in the US and that government spending has gotten out of control. According to statistics from the Board of Governors of the Federal Reserve System, from January 2020 through November of 2021, the United States has printed nearly 80% of all US dollars in existence. Additionally, the US continues to pile on debt, feeding concerns about partisan congressional views on the budget and the recurring debate over the debt ceiling that has threatened to shut down government spending. These issues cause some to question the stability of the US’s financial infrastructure and therefore the future of the USD’s status as the global reserve.

Weaponization of the US Dollar

Perhaps the loudest argument in favor of the USD’s demise as the global reserve centers around the so-called weaponization of the dollar. This argument gained force in February 2022, when over $300 billion in Russian foreign reserves were effectively frozen by the US and its Western allies after Moscow invaded Ukraine. This freezing of accounts combined with sanctions on Moscow and the country’s oligarchs has forced Russia to switch trade to other currencies and increase its reserves of gold. The yuan has since reportedly replaced the U.S. dollar as the most traded currency in Russia, according to Bloomberg.

Some argue that these sanctions have fueled fear among other countries for their own dollar stores abroad, worrying that any disagreement with US foreign policy could result in having assets confiscated or frozen.

Even US Treasury Secretary Janet Yellen has acknowledged the risk of sanctions, telling CNN in April: "There is a risk when we use financial sanctions that are linked to the role of the dollar that over time it could undermine the hegemony of the dollar." While sanctions are, she noted, an “effective tool…[they do] create a desire on the part of China, of Russia, of Iran to find an alternative.”

These sanctions have led to growing concern abroad that the dollar may become a permanent political tool or be used as a form of economic statecraft to exert pressure on countries to enforce sanctions they may disagree with.

As a currency’s reserve status depends upon its convertibility, liquidity and the ability to move money in and out with ease, if widespread sanctions or the freezing of assets make that impossible, it raises alarm bells around the reserve currency’s ability to achieve its desired function.

While there has been a lot of noise in the wake of Russian sanctions, an analysis of the broader effects of these sanctions yields an arguably less alarming picture. If we go back around 30 years, sanctions on countries for various activities by the US and Western allies affected around 10% of countries globally. That percentage has grown over the years, and by some measures now touches 30% of all countries in some fashion. However, most of the economies affected are in transition and not currently very meaningful to the financial system, including countries like North Korea, Iran, Venezuela, Cuba, Syria, etc. The additional sanctions are also tied to a fairly small number of issues, such as the export of ammunitions and munitions to Afghanistan, that would not affect the majority of economies.

The recent sanctions imposed by the West on Russia are arguably the exception that proves the rule. Given that Russia’s invasion of Ukraine has sparked the first hot war in Europe since 1945, the US and its Western allies’ response should perhaps not be viewed as a departure from or escalation of previous foreign policy initiatives but rather consistent with the West’s protection of national sovereignty that has defined its foreign policy ethos since World War II. Should the US start imposing sanctions more liberally or broadly or imposing them unilaterally, then one could argue this notion of the weaponization of the US dollar should be more worrying to the international community.

That being said, there is no denying we are moving from a unipolar to a multipolar world. And countries like China and Russia that are staunch political opponents to the US are justifiably concerned about the extent to which this so-called weaponization may impact their economies’ access to international financial markets. Countries like Saudi Arabia and Iran are similarly positioned. However, the long history of alliance between Washington and Riyadh is unlikely to completely unravel anytime soon, and analysts don’t anticipate a break away from dollar-denominated oil trade over the short-term.

Janet Yellen pointed out in her CNN interview that while intent to move away from the USD may be there for countries like Russia and China, it is not easy to replicate the currency ecosystem — such as the international payments infrastructure — that supports the US dollar, and therefore a more widespread migration away from the US dollar for trade settlement is difficult to achieve.

Should the US dollar however become a permanent political tool in the context of US foreign policy, then perhaps we should start to question its status as the dominant reserve and trade currency. But so long as these sanctions are used sparingly and multilaterally, there is less of a risk that the weaponization of the USD will be seen as such a threat for a meaningful contingent of countries to significantly change their mix of foreign exchange reserves.

Taking a look at history

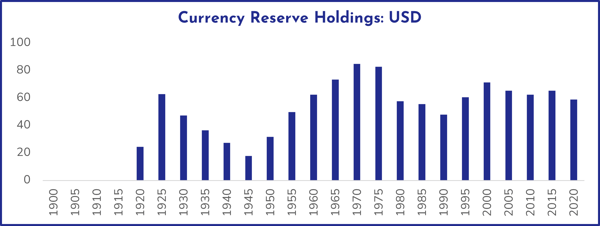

This is hardly the first time in history that people have been calling for the dollar's demise. There has been a keen focus on most recent 20-year decline of the USD in its reserve share from above 70% to around 58%. But if we take 100 years of history, then the USD’s current level doesn’t look quite as alarming.

For example, when the dollar was at its very strongest in terms of value in 1985 just before the Plaza Accord, its percentage of total reserves was 55.6%. In 1920, the USD accounted for just 24% of global reserves, and by the end of the Second World War in 1945, it was only 17.9%. It was in the wake of the Bretton Woods agreement post the Second World War that the US dollar began its ascent to pre-eminence and hegemony. From its low in 1945, it rose to its zenith in 1970 of 85% but then declined again through the 80s and 90s into to a level in 1990 of around 48%.

Source: IMF, Barry Eichengreen, 2014, “International Currencies, Past, Present and Future: Two Views from Economic History”.

So the USD’s share of the total global reserves has varied significantly over the decades, suggesting this most recent decline is perhaps not as alarming for the dollar or for the global economic balance as some are predicting.

It is also worth noting that the relatively steep decline we saw in the dollar’s reserve percentage in 2022 can be almost entirely attributed to the falling value of US Treasuries and not to a divestment of them. Foreign holders of US Treasuries in 2003 stood at $1 trillion; that figure is now at $7 trillion, so there is at this stage no meaningful indication of an exodus in demand.

Crucially, there is no correlation between the direction of the dollar and the size of dollar reserves, so a decline in reserve status does not predict a loss in value. There is in fact more evidence to suggest that a decline in the dollar’s value increases its percentage of reserves because quite a few particularly emerging economies tend to accumulate more dollars when the currency is softening, as their central banks try to resist domestic currency appreciation. These reasons all suggest that perhaps this 20-year trend of decline in the US dollar’s reserve share is not the death-nell for the dollar that some predict.

What are the criteria for a reserve currency?

In order for a currency to be able to act as a global reserve, its economy needs to be of sufficient size and its capital markets need sufficient depth in order to issue enough currency for other countries to hold and trade.

A reserve currency also requires liquidity, openness of capital markets and convertibility to allow market participants to be able to trade in and out of those assets with ease and to quickly convert the currency, particularly in times of stress.

Sound property rights and general faith in the rule of law are also critical, so that market participants believe their assets cannot be easily sequestered.

There are not many economies around the world that currently have all those attributes. The US is arguably the only one.

Is there a viable alternative?

Looking at the euro area, the total size and depth of its capital markets is not comparable to the US, particularly for triple A-rated securities.

Meanwhile, while diversification of assets in reserve accounts over the last ten years has increased exposure to certain other G10 currencies, like the Australian dollar and the Canadian dollar, their percentages of reserve holdings are still below 5%. Sterling is now upwards of 5% of reserves, and the Japanese yen is about 5%. But these are all still relatively quite small, and none of them has the ability to challenge the US in terms of size and depth of capital markets.

Gold has risen in terms of its percentage of holdings, but it is a small player with a total market size of around $11 trillion, whereas the debt securities market alone in the US is $50 trillion.

China is arguably the only economy that currently has the size and depth to compete for its currency having reserve status. However, there are a number of factors working against the Chinese yuan in this regard. The first is capital controls: China’s capital markets are not nearly open enough to facilitate the type of trade that would be required for the yuan to be the global reserve. There is also a convertibility issue: the Chinese cross-border payments system is still quite small compared to CHIPS, and there is a limit to what you can actually own in yuan, as it does not have a deep FX market in bilateral currencies except with the USD.

There is also an important distinction between bilateral and multilateral trade. While it is reasonable to assume that trade with Beijing will rise and will increasingly be invoiced in yuan, that is a relatively small issue on the global stage and will very likely be confined to bilateral trade. Is it likely, for example, that Middle Eastern exporters and African importers will start invoicing their exchanges in yuan? That type of yuan-based multilateral trade seems unlikely at this point.

What about central bank digital currencies? China is for the time-being at the forefront of that initiative with E-CNY, its digital currency. It is however unlikely that E-CNY will have any effect on reserve currency balances, as the digital currency’s primarily objective is to challenge Tencent and Alipay’s roles in payment systems and to provide additional surveillance on Chinese citizens. It does not address China’s fundamental capital control issues. There are 110 central banks currently looking into CBDCs, so it is a space to watch. But we believe their viability as potential reserves will ultimately depend on the currency and economy each is tied to.

Cryptocurrencies also get a lot of attention for their potential to replace fiat currencies, with some viewing Bitcoin as a hedge against the USD, should the dollar experience a precipitous decline. There are however five major problems with cryptocurrencies as potential reserves: volatility is too high, credibility is too low, liquidity and market size are too small, and correlation with risk assets is too high. An attractive reserve currency will often be a safe haven in times of risk asset decline, but recent history has shown that cryptocurrencies have suffered in line with markets in times of financial stress. So it is much too early to believe that cryptocurrencies are a viable alternative to the USD as a global reserve. The cryptocurrency space is still however in its very early stages, and its ultimate impact upon financial markets is still unknown.

Are we being too complacent about dollar dominance?

It is probable that in time the dollar's share of global reserves will decline further. As we evolve into an increasingly multipolar world, more trade will be conducted in other currencies. Ideological tensions are rising across the globe, and the democracy versus autocracy divide will inevitably lead to changes in the patterns of global trade and, to a degree, the holdings of global currency reserves. But we believe any near-term change in the breakdown of global reserves will be at the margins and will not meaningfully disrupt the current economic balance.

Even if the USD does slip below 50% of total reserves, it would still very much be the dominant reserve currency, as no other currency comes close to approaching those levels. The yuan would have to rise exponentially from its 2.5% level to contemplate even getting close to the USD’s share. While the direction of travel for the USD’s share of global reserves may continue to be down, it is very likely to be gradual and is unlikely in and of itself to impact the direction of the dollar. The dollar’s value will continue to be determined by underlying economic fundamentals – valuation and the cyclical economic interaction of countries and regions – which is a separate subject entirely from the reserve and trade currency discussion.

It is also worth taking into account the large number of currencies currently pegged to the USD, including most of the Caribbean islands, countries in the Middle East including Jordan, Oman, Qatar, Saudi Arabia, and the UAE, and in Asia, Macau and Hong Kong. Smaller countries peg their currency to the USD to help stabilize and secure their economies to protect them from volatility, while for oil-rich countries, pegging to the dollar adds stability given their important trading relationship with the US. Should we begin to see a number of these currencies removing their dollar peg, perhaps that creates greater scope for a challenger to the USD as global reserve, but there is currently not a lot of evidence to suggest that will happen anytime soon.

However, the US dollar’s status is not bullet proof.

This status as the global reserve and trade currency is predicated upon widespread trust in the US’s institutions and in its ability to repay its debts. If the US were to abuse the use of sanctions, run consistently bad macro policies, become isolationist, or default on its debts, then trust in its institutions and faith in its government’s credit would likely erode and undermine the US dollar’s hegemonic status. Although, we don’t view those outcomes as likely in the near term.

In summary, looking through the lens of history and evaluating what has driven the dollar's resilience thus far, we would argue that imminent demise is not around the corner for the greenback. However, longevity is not immortality, and there are longer-term risks to the USD’s current status as the dominant reserve and trade currency should the US make decisions that would erode trust in its institutions and creditworthiness. Given the current macroeconomic landscape, however, any potential further decline in status for the US dollar is likely to be gradual and to not send immediate shockwaves through global markets.

The views and opinions contained in this document are those of Abigail Cushing and Mark Astley, correct as of April 2023 and does not necessarily represent the views and opinions of Millennium Global or any of its Portfolio Managers. This information is intended for Professional Clients only, not retail clients. This information does not constitute an offer to buy or a solicitation of an offer to sell and does not constitute an offer or solicitation in any jurisdiction in which such a solicitation is unlawful or to any person to whom it is unlawful. Please see Important Disclaimers on: https://investments.millenniumglobal.com/millennium-global-marketing-disclaimers

Taking on the future: Machine Learning in FX Risk Management

By Justin Gang Xu, Head of Risk The global foreign exchange markets are primarily influenced by a combination of fundamental and market dynamic...